Section I: Background

The Securities and Exchange Commission (SEC) is in the rulemaking process for The Enhancement and Standardization of Climate-Related Disclosures for Investors, a rule that would mandate comprehensive and comparable disclosures from public companies. Requiring disclosures of this type is well within the scope of the SEC’s mandate to support investors in their decision making, ensure fair and efficient markets, and enable capital formation.

The financial risks posed by climate change to all market participants are well documented by numerous government studies. Many investors already take climate into account, and companies in turn rely on a wide variety of voluntary initiatives and accounting standards to provide them data. By seeking to standardize reporting–which investors have long called for– the SEC is providing investors and other market participants with clear, consistent, and comprehensive information they need.

As investors and engines of capital allocation, banks stand to benefit greatly from the standardization of climate-risk disclosure–and to be harmed by the continued regime of incomplete, flawed, and non-comparable data. Some bank executives have voiced mild support of the SEC’s disclosure rule, including executives from Morgan Stanley, Bank of America, and Goldman Sachs. However, banks have largely remained silent during rulemaking. In early May, Bank on Our Future asked the six largest US banks, all of whom are voluntary members of the Net Zero Banking Alliance (NZBA), a series of questions, including whether they planned to send official comment on the rule before the comment period ends on Friday June 17th. While executives from a few of the “Big Six” did respond, all declined to directly respond to our question or commit to commenting. Citigroup referred us to its Taskforce on Climate Financial Disclosures report, which repeatedly claims the bank will support policies like the disclosure rule. JPMorgan Chase also referred us to its TCFD report, which will not be available until the end of 2022.

Remaining silent on a baseline climate disclosure rule is counter to explicit commitments made as members of the NZBA, as well as other commitments these banks have made to achieve net-zero operations. For instance, the NZBA commitment explicitly states that signatories will engage in “corporate and industry (financial and real economy) action, as well as public policies, to help support a net-zero transition of economic sectors in line with science[.]” By standardizing the provision of clear, consistent, and comprehensive data on the climate-related financial risk companies face, the SEC’s disclosure rule is precisely the kind of public policy NZBA signatories committed to engage with.

It should be noted that in addition to the Big Six, we sent our letter to all members of the NZBA’s Steering Group. Amalgamated Bank, which serves on the Steering Group, did engage with our questions. Among other things, Amalgamated was the one bank that confirmed to us their plans to submit an official comment.

We hope to bring much-needed scrutiny to the banking sector’s general silence on the SEC’s rule, especially in the face of individual banks’ numerous voluntary net zero and other climate commitments AND the lobbying efforts done in their name by The US Chamber of Commerce to sink the rule. The following analysis follows one simple line of questioning: if banks who have made net zero pledges and commitments to disclose climate risk cannot agree to publicly support the most basic policy to enable an economy-wide net-zero transition, then when will they? Are their calls for policy action simply hollow gestures to shrug off their own responsibilities? And if voluntary structures like the NZBA cannot hold banks to their own basic commitments, what authority do they have, and can they be viewed as anything but greenwash as banks in reality continue to pour money into the fossil fuel industry?

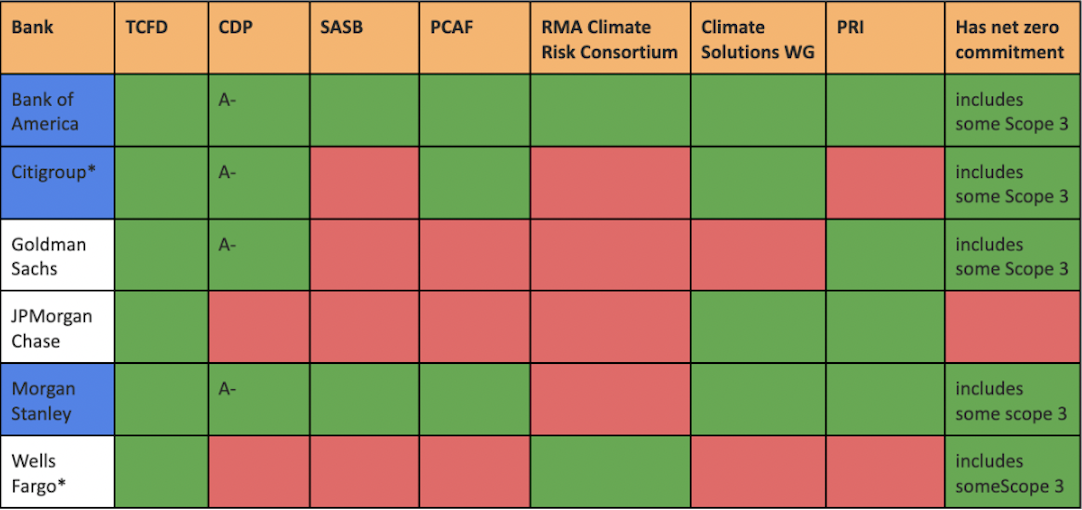

Section II: The voluntary agreements

Below is a matrix demonstrating some of the signature net zero, environmental governance, and sustainability commitments that each of the Big Six belong to (green) or not (red), and, where applicable, ratings or grades they have been awarded. All of the listed banks belong to the NZBA. The banks highlighted in blue serve on the NZBA’s Steering Group.

The voluntary agreements are the:

- Taskforce on Climate Financial Disclosures (TCFD), an initiative of the Financial Stability Board to provide guidance and resources for company disclosure of climate-related financial data. All of the banks report to the TCFD, and JP Morgan Chase and Citi referred to their TCFD reports in their responses to our questions. The SEC climate disclosure rule is based on the TCFD.

- Carbon Disclosure Project (CDP), a UK-based organization that houses a “global disclosure system for investors, companies, cities, states and regions.” It provides a grading for company disclosures.

- Sustainability Accounting Standards Board (SASB), a global reporting framework, maintained by the Value Reporting Foundation, that guides the “disclosure of financially material sustainability information by companies to their investors” across 77 industries.

- Partnership for Carbon Accounting Financials (PCAF), an industry-led initiative that has innovated a groundbreaking standard for greenhouse gas accounting and reporting for banks and other financial institutions.

- RMA Climate Risk Consortium, a project of the Risk Management Association, a banking trade group. Launched by Bank of America’s Mary Obasi in 2021, it brings together 33 financial institutions from around the world to help banks develop strategy around, disclose, and manage the risks of climate change.

- Chamber of Commerce’s Climate Solutions Working Group (Climate Solutions WG), an informal group within the US Chamber of Commerce that serves to engage the Chamber on climate policy.

- Principles for Responsible Investment (PRI) signatories agree to a set of six voluntary principles to make ESG principles part of investment practice.

(*Both Citigroup and Wells Fargo included absolute targets for emission reductions in their plans, limited to the energy sector. This represents higher ambition than intensity targets, which continue to be the dominant paradigm.)

Signatories to the NZBA commit to framing plans to achieve net-zero emissions and to support policy that enables the transition to a low-carbon economy. Not all of the additional listed voluntary commitments support rigorous disclosure, and not all of them recommend or require engagement in the policy process as criteria for belonging. However, banks have been consistently on the record saying that voluntary commitments alone are insufficient, and that policy makers must also pave the way. Despite having all committed–in multiple forums–to the principles of disclosure as fundamental to a net-zero pathway, the Big Six seem to be letting the opportunity to publicly engage on a rule that would simplify, clarify, and standardize disclosure pass them by.

In addition to the NZBA, membership in the following initiatives would suggest support of policies like the SEC’s disclosure rule.

PCAF’s Commitment Letter suggests that standardizing greenhouse gas accounting methodologies in the near term is crucial and that financial institutions must report not just on their Scope 1 and 2 emissions, but also the emissions they finance. That kind of clarity and standardization is exactly what the SEC’s rule seeks to create. The letter declares, “Addressing the urgent challenge of climate change, and decarbonizing our economy, is more pressing now than ever. That is why we have committed to measure and disclose the greenhouse gas (GHG) emissions associated with our portfolio of loans, investments, insurance liabilities and other financial products and services within a period of three years using jointly developed GHG accounting methodologies, in order to ultimately enable the alignment of our portfolio with the Paris Climate Agreement.“

TCFD’s 2022 Overview includes the initiative’s “Fundamental Principles for Effective Disclosures,” which also tracks with the objectives of the SEC’s proposed rule. Among others, TCFD’s principles state: Disclosures should represent relevant information, be specific, complete, and clear, and they should be comparable among companies within a sector, industry, or portfolio.”

Disclosures that communicate “in a common voice to regulators” as well as “assessing/preparing for regulatory disclosures” are one of the three primary initiatives of RMA’s Climate Risk Consortium. The Consortium has engaged with the regulatory rulemaking process on issues like this in the recent past, having submitted a comment that was broadly supportive of the Office of the Comptroller of Currency’s draft rule on the management of climate-related financial risk by big banks. Additionally, among the six “voluntary and aspirational” principles that PRI signatories agree to, three suggest active engagement in the policy process as “possible actions.”

Section III: What the banks have said

In official documents (e.g. TCFD reports) and public statements from corporate representatives, five of the Big Six have voiced either direct support of the rule or support for strong public policy like it.

Morgan Stanley

Chief Sustainability Officer Audrey Choii called the SEC rule “incredibly prolific” and “amazing” in terms of signaling to chief risk and financial officers that non-sustainable behavior has consequences. “Clearly … regulators have seen that climate is a risk factor to business that cannot be ignored,” she said. “You cannot be a responsible business presenting what you believe to be your financial statements and your risks and opportunities in a clear, transparent, and reliable way without at least considering [climate risks]. … No savvy investor is going to want to make investments without being able to have comparable transparent data to make that judgment on.”

In its 2020 TCFD report, Morgan Stanley claimed it “supports policies that will help accelerate the transition to a low-carbon economy and will continue to engage with policymakers and other industry groups as opportunities arise to support the development of effective regulatory policies to address climate change.”

Bank of America

Head of Sustainability Paul Donofrio told Reuters, “We think the proposal is constructive and headed in the right direction… We are all in on this notion of companies providing the marketplace with disclosures that will help everybody understand what the emission status is at a company and what their plans are to get to net zero … so that market participants can allocate capital to the best and highest use.”

Karen Fang, Global Head of Sustainable Finance, argued for standardization and clarity on Scope 3 to SPG Global, saying, “For us, as a bank, the biggest challenge is Scope 3 because that’s our entire supply chain and value chain…It really takes all of our clients that we lend money to and invest in to work with us on a credible transition plan to transition to net zero so our financing and investment emissions — which is the biggest contributor of our Scope 3 emissions — can be neutralized over time.”

Directly addressing the SEC Rule, Fang said, “At BoA, we have been a long term supporter of transparent ESG disclosure and stakeholder metrics disclosure…The overall direction of travel is right…We have to be very cognizant of the fact that Scope 3 emissions include your entire value chain. The data needs to be better… the accuracy needs to be improved. There are still too many idiosyncracies… We need to have some safe harbor solutions” while the data problems improve.

In its 2020 TCFD report, Bank of America claimed, “We are supportive of policies that will help accelerate the transition to a low-carbon economy…We are working with and within the US Chamber of Commerce, Business Roundtable, and other trade associations of which we are a member to encourage more urgent action on climate change from the public and private sectors.”

Citigroup

Citi repeatedly emphasized the need for strong enabling policy and its commitment to supporting it: In its 2021 TCFD report highlights document, Citi claimed, “We recognize that in addition to private sector action, a net zero future will also require public policy and technology solutions, which we will actively support. While we acknowledge that fully transitioning the global economy will take decades, we understand the urgent need for near-term actions that will deliver the rapid emissions reductions required.”

In its 2021 TCFD Report, the bank emphasized the need for strong, enabling policy on multiple occasions, claiming that:

- “There is a critical need for strong public policy to accelerate the global economy’s transition to net zero.”

- “We know, however, that it will not be possible to achieve a net zero global economy without strong and enabling climate policy across key jurisdictions, and it is part of our net zero plan to support these policy advancements as well.”

- And committing itself to,“support enabling public policy and regulation in the United States and other countries, including through trade associations and other industry groups.”

- “A lack of global regulatory clarity, or cohesion, on climate and other sustainability matters also adds to the challenges Citi faces as we undertake our net zero plan. To help address this, we hope to work in tandem with regulators to enable climate policy, particularly in higher-emitting countries, by helping to provide support to achieve more ambitious decarbonization goals in these jurisdictions.”

Citi’s TCFD report explicitly names involvement with the Chamber of Commerce’s Climate Solutions Working Group. It says that, “Engagement includes discussion of the Chamber’s positions on climate change and shared interests among Chamber members in climate-positive technologies, climate policy solutions, and other related initiatives. In October 2021, the Working Group posted a statement urging the Chamber to take action on comprehensive legislation to help business accelerate the transition to a decarbonized economy. The statement recommended the development of policies to support options such as carbon pricing to drive development of emerging technologies, low-carbon infrastructure and carbon capture and sequestration programs.”

Goldman Sachs

When asked directly about the proposed rule, Catherine Winner, global head of stewardship at Goldman Sachs, told the Wall Street Journal, “Our voting framework is very supportive of the SEC’s proposed climate-risk disclosure rules. Both the SEC and the TCFD are really pushing for greater emissions disclosures grounded in materiality…In the U.S. particularly, our policy will support progress on emissions reporting as we get closer to the proposed implementation deadline for the SEC’s rule…”

In its TCFD report from 2021, Goldman Sachs suggests it is supporting policy like the proposed rule, claiming that, “Supportive public policy and technological advancement will be critical for financial institutions to effectively engage corporates in these sectors in transition and invest in new solutions. Further, accelerating policy action will be a key determinant in driving the pace at which we and our clients can achieve decarbonization goals across sectors and geographies.” Additionally, it said that the “Global transition to a low-carbon economy will require a supportive policy environment, and in some cases, accelerated policy action to support the orderly transition of industries and sectors. In early 2021, we joined Inevitable Policy Response (IPR) as a strategic partner, alongside several other financial institutions.”

After the SEC’s rule was proposed, a report with a generally neutral tone said that, “The aim of the proposed rule is to improve the consistency, quality and comparability of company-reported” emissions… in “an effort to standardize costs in reporting of climate-related metrics and targets, all while improving consistency, comparability and ease of access for investors… enabling investors to more effectively incorporate these risks and opportunities into their fundamental assessments while simplifying and clarifying the reporting expectations for companies… These rules would represent a higher bar, not only for US companies but foreign issuers listed in the US.” It dismissed criticisms of the costs and burdens of reporting, saying that, “Companies already disclosing robust climate-related data, particularly those with assured emissions figures (employing Greenhouse Gas Protocol standards) and/or TCFD reports are least likely to see any increased reporting cost burden should this proposed rule be adopted by the SEC.”

Wells Fargo

Unlike the previous four banks, Wells Fargo has not voiced any kind of strong support for standardized or mandatory disclosures.

In its 2020 TCFD report, the bank seemed to suggest that an acceleration in data quality and standardization was necessary to improve disclosure, “Many gaps exist in our ability to calculate the financed emissions of our portfolio due to the lack of comprehensive, integral data. We support efforts to improve the monitoring, reporting, and verification of GHG emissions through data-driven innovations such as machine learning and artificial intelligence, remote sensors and satellites, and advanced geospatial image processing.” The bank indicated that it is open to both voluntary and mandatory disclosure to provide their investors with useful information. It said, “Utilizing frameworks to standardize climate-related disclosure supports the accountability aspect of long-term, effective climate action. We are guided by mandatory and voluntary disclosure frameworks as we engage in a meaningful dialogue that provides our stakeholders with consistent, standardized information.”

JPMorgan Chase

JPMorgan Chase has essentially said nothing public about the need for better disclosure or its commitment to pushing for better policy. In private communication with us, bank representatives told us that more information would be available when they release their TCFD report later this year.

Section IV: Why comments and public support are crucial right now

In rulemaking, the public comment period is a crucial time. Not only do comments, data, and recommendations help shape an agency’s final version of a rule, those comments are extremely useful in validating the scope and ambition of a rule. When an SEC commissioner is questioned publicly or in a hearing about aspects of the rule, being able to point to public comments, especially from key stakeholders (e.g. relevant industry voices), is critical. Comments will also be extremely useful when officials must defend the rule against litigation that is inevitable for rules of this type.

By not going on the record now, parties that have an interest in the rule are choosing not to engage in the process publicly, not to pursue a relatively simple avenue to ensure their values are reflected in regulations that would directly apply to them, and casting doubt about the seriousness of other public statements and actions that suggest support for the rule in question.

As we have stated before, it is not unusual for banks to comment during rulemakings, as Bank of America did for the Office of the Comptroller of the Currency’s recent rule. Amalgamated Bank expects to comment on the SEC disclosure rule. Numerous financial companies have already submitted comments, including Deloitte, Rockefeller Asset Management, Decatur Capital Management, Other companies, including Deloitte, Overstock.com and Allbirds have also submitted comments.

One of the strongest opponents of the rule has been The US Chamber of Commerce (The Chamber). In line with its long history of siding with its fossil-fuel industry members over the interests of others, The Chamber has engaged in vigorous lobbying against a strong climate disclosure rule since before the release of the draft rule. After the rule was released, it led the opposition response in the media, with its Executive Director Tom Quaadman quoted across the media. The Chamber submitted a letter in April calling for an extension of the rule and offering extensive critique of the rule, in particular its aim to gather data on firms’ Scope 3 emissions.

As noted in Section II, four of the Big Six banks belong to The Chamber’s “Climate Solutions Working Group,” a voluntary initiative that seeks to “engage” The Chamber on climate-related issues. In October 2021, some members of the Working Group sent a letter urging Congress to pass climate legislation. If they are working to engage The Chamber on the SEC’s disclosure rule, they should indicate as such and be prepared to make public statements of dissent.

It would be one thing for banks to remain silent and neutral during this comment period. But to remain silent while an industry group to which they pay dues actively seeks to gut the rule should come with consequences. These are banks that regularly tout their many voluntary agreements and commitment to net zero. They are the same banks whose corporate social responsibility executives regularly seek adulation and whose marketing strategies often feature their awareness of climate change. They are the same banks that regularly say their hands are tied until policies that enable them are passed and standardized.

So we ask when. When will you begin to actually support the basic policies and regulations that must be in place? When will your efforts to move meaningful public policy match your stated commitments for it? And when will the voluntary commitments you’ve made–as well as the people who steward them–require you to translate your verbal commitments to practice?